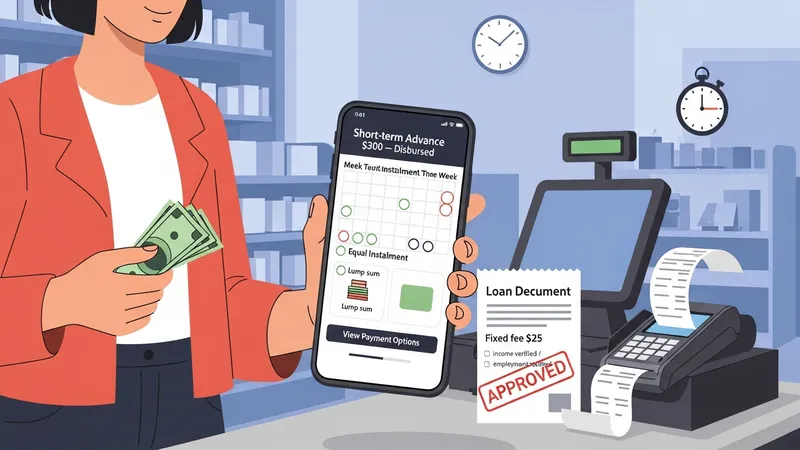

Short-term financing that delivers cash up front with scheduled repayment over weeks to months is a category of consumer credit characterized by rapid disbursement and condensed repayment timelines. These arrangements generally provide small principal amounts relative to traditional personal loans, and they often combine a fixed fee or short-term interest with defined installment or lump-sum repayment. Lenders or platforms that offer this format may assess income, employment stability, or account activity quickly to support faster decisions than many longer-term lending products.

Such near-term credit structures can be offered at point of sale, through mobile platforms, or by specialist lenders. They can differ from revolving credit in that the obligation is typically a one-time advance with a finite repayment schedule rather than an ongoing credit line. Consumers and analysts commonly distinguish these products by factors such as origination speed, fee structure, whether installments are equal or graduated, and whether early repayment changes total cost.

When comparing these example structures, it is useful to consider how approval criteria and processing times may differ. Point-of-sale deferred payment plans often require minimal underwriting and can be approved in real time, while some installment products may use more detailed income verification and can take longer to fund. Fee disclosure, short-term annual percentage rate (APR) equivalent, and repossession or collection policies for missed payments are variables that may vary by provider and by jurisdiction. Consumers and researchers often examine sample repayment scenarios to understand effective costs across formats.

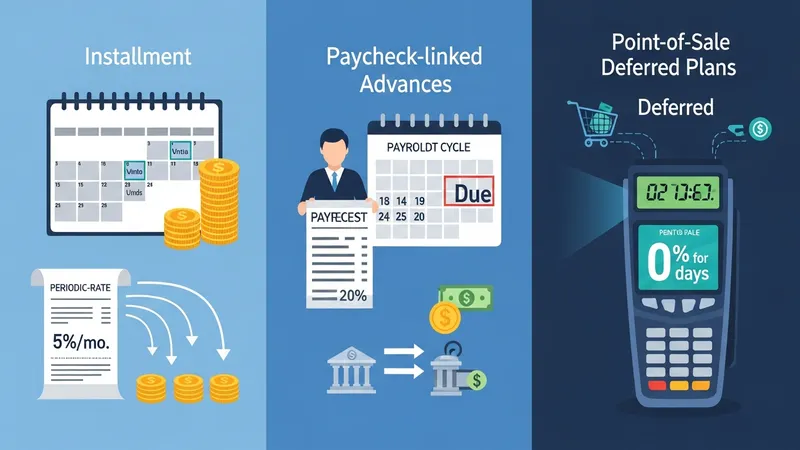

Repayment scheduling patterns typically fall into two general groups: equal periodic installments and backloaded or balloon-style payments. Equal installments split principal and any interest or fees into recurring payments due weekly, biweekly, or monthly, which can aid predictable budgeting. Backloaded schedules may reduce near-term outflows but often increase total cost exposure if interest accrues. For payroll-linked advances, repayment alignment with pay dates may reduce short-term strain but can concentrate outflows on the next pay period, which is an operational consideration for household cash flow modeling.

Cost components for these short-term advances often include explicit finance charges, origination fees, or flat service fees, and may be expressed as APRs or as per-transaction fees. Fees that appear modest in absolute terms can translate into high short-term APR equivalents when the term is brief, so it is common to compare both nominal charges and their time-adjusted impacts. Providers may also charge late or returned-payment fees that increase the total amount due if scheduled payments are missed; these secondary charges are relevant to risk assessment and planning.

Risk and consumer protection aspects vary by jurisdiction and provider type. Regulatory frameworks in many areas impose disclosure requirements, caps on certain fee types, or rules on collection practices, and those frameworks can affect both product design and cost. Credit reporting, eligibility impacts, and the presence or absence of hardship or dispute-resolution processes are additional considerations that may influence longer-term financial outcomes. Analysts often recommend reviewing contractual terms and hypothetical repayment scenarios to evaluate potential exposures.

In summary, immediate-disbursement short-term advances are a diverse set of credit arrangements that combine quick funding with compact repayment schedules. Differences in underwriting, fee structure, repayment mechanics, and regulatory treatment mean that comparable headline charges can have different practical implications for cash flow. The next sections examine practical components and considerations in more detail.

Short-term cash-forward financing comes in multiple structural forms that may suit different purchase contexts or timing needs. Installment advances divide repayment into a set number of scheduled payments and often include a finance charge expressed as a periodic rate or a flat fee. Paycheck-linked advances connect repayment to payroll cycles and can reduce the need for frequent transfers but may concentrate liability on a single date. Point-of-sale deferred plans can be interest-free for brief promotional periods or carry fees that activate if the balance is not cleared within the promotion window. Each structure typically prioritizes speed and convenience over duration.

Providers choose structures that balance underwriting burden with customer access. Minimal-document offers may approve small advances rapidly based on automated checks, while products that offer larger amounts typically require more documentation. Promotional point-of-sale options are often integrated into merchant checkout processes and may rely on third-party underwriting platforms. From a consumer perspective, understanding whether the product is a true installment obligation or a deferred single-payment obligation clarifies the timing of principal reduction versus fee accumulation.

Common features across structures include automated repayment initiation, options for early repayment, and specified consequences for missed payments. Automated transfers reduce operational friction but require confirmation of payment sources and calendar alignment; users may find that scheduling conflicts with bank holds or payroll timing can cause inadvertent misses. Early repayment options often reduce future interest accrual, but some contracts include prepayment fees or do not adjust flat fees, so contract terms should indicate whether early payoff materially changes the total amount due.

When evaluating these structures, a practical consideration is how typical use cases align with household cash flow cycles. Short-term advances may fit short timing gaps between expenses and incoming funds but can also create concentrated repayment obligations that intersect with other periodic bills. Modeling several repayment timelines can reveal stress points where multiple obligations coincide. These alignment considerations are often as consequential as headline pricing when assessing practicality.

Approval processes for quick-disbursement credit tend to emphasize speed and low friction, relying on automated data sources and simplified verification. Common inputs include recent income deposits, bank transaction patterns, employment indicators, or basic identity checks. Some providers use soft checks that do not impact credit files; others perform hard inquiries or report performance to credit bureaus. The depth of verification typically correlates with the amount requested: smaller advances may be approved with minimal documentation, while larger short-term lines can trigger more traditional underwriting steps.

Affordability assessment methods may vary and can include simple debt-to-income comparisons, analysis of recent account flows, or algorithmic assessments of repayment capacity. These approaches can reduce manual review time but may also miss context-specific factors. For example, a temporary dip in account balances might be treated differently by a human underwriter than by an automated rule. As a result, applicants can see inconsistent outcomes across providers depending on data inputs and thresholds used in decision models.

Timing of decisions is a central feature: many platforms aim to confirm approval within minutes and disburse funds within the same day. That speed can be helpful for short timing gaps but may increase the risk of accepting terms without thorough comparison. Providers may impose limits on repeat borrowing or require a cooling-off period between successive advances. These operational controls are often part of risk management and may impact how frequently someone can access short-term advances.

Insider considerations for users and analysts include checking whether approval involves recurring permissions such as continuous access to bank data and whether the provider reports account activity to credit repositories. Reporting can influence longer-term credit profiles. Additionally, some underwriting models prioritize recurring deposit patterns, so irregular income types may require alternative documentation. These distinctions can affect both eligibility and downstream credit reporting outcomes.

Repayment schedules for short-term financing typically range from a single due date within a few weeks to several monthly installments over a few months. The schedule chosen affects how finance charges are calculated and how quickly principal is reduced. Equal-installment schedules spread principal and finance charges evenly, which may simplify budgeting, while single-payment or balloon schedules may defer principal reduction and concentrate cost in the final payment. Providers also vary in whether they allow payment by debit, ACH, card, or payroll deduction, which can influence timing and returned-payment risk.

Cost factors include explicit finance charges, origination or service fees, and potential penalties for late or returned payments. Because terms are short, nominal fees can correspond to high APR equivalents; describing costs both as total dollars charged and as time-adjusted rates can provide clearer context. Some plans offer promotional periods with no fees if the obligation is repaid within a prescribed window; failure to meet those conditions often triggers retroactive fees or interest, increasing total cost compared with the promotional statement alone.

Fee timing and accrual methods also matter. Flat fees assessed up front increase the effective principal immediately, while interest that accrues over the term affects the outstanding balance differently. Prepayment mechanics vary: some contracts recalculate finance charges on the outstanding balance if paid early, while others retain flat fees regardless of repayment timing. These structural choices can materially affect the amount ultimately repaid and therefore are important to compare in hypothetical repayment scenarios.

Practical considerations include aligning repayment dates with income cycles and confirming whether autopay can be paused in the event of a dispute or hardship. Cash flow simulations that layer short-term advance repayments with other recurring obligations can highlight potential pinch points. Additionally, monitoring for returned-payment fees or late notices is important, as cascading fees and collection activity may raise overall cost and administrative burden beyond the original agreement.

Planning for short-term advances involves assessing likely repayments alongside existing financial commitments and contingency plans for unplanned events. Risks include payment concentration when several obligations fall in the same period, potential bank account holds or returned payments, and the cumulative effect of repeated short-term borrowing. Consumer-protection frameworks in different jurisdictions commonly mandate clear disclosure of total charges, but terms and enforcement can vary. Reviewing contractual dispute and hardship provisions may clarify options if repayment becomes difficult.

Repeated reliance on short-term advances can create a cycle where forthcoming obligations reduce available liquidity for subsequent needs. Many analysts note that this pattern can emerge when advances are used for recurring gaps rather than one-time timing mismatches. Monitoring cumulative outflows and tracking the frequency of borrowing events are practical steps that may reveal whether short-term advances are occasional tools or an ongoing component of cash management.

Insider details to consider are the extent of credit reporting and collections procedures associated with a product. Some providers report only defaults, while others report full payment histories; both approaches influence future access to other credit products. Collection timelines, dispute-resolution mechanisms, and whether a provider participates in any industry codes of conduct are additional factors that can affect long-term outcomes. Understanding these procedural aspects can reduce surprises if repayment problems arise.

Overall, short-term cash-forward advances serve specific timing needs but carry trade-offs related to cost and repayment concentration. Evaluating hypothetical repayment scenarios, understanding fee mechanics, and considering how these advances interact with broader financial obligations are central planning steps. For readers continuing through the article, subsequent material offers further detail on operational mechanics and comparative frameworks for assessment.